Tell someone you’re starting a business, then brace yourself for their overwhelming show of support:

Wow, 95% of all businesses fail, right? That’s scary.

Most businesses are never profitable and fail within 5 years. That’s mind-blowingly depressing. Aren’t you worried about all the time and money you’ll lose?

So many businesses end in bankruptcy. Aren’t you worried about that wrecking your life?

I don’t think that’s a good move in this economy. (Right Dale?)

Well actually, these “well-known facts” are crap.

For example, let’s examine that 95% failure rate. The United States Department of Labor reports that the number of business that terminate within four years is just 24%. And for only 17% of those, “termination” meant failure or bankruptcy — the majority were businesses that were sold or the owner retired.

For example, let’s examine that 95% failure rate. The United States Department of Labor reports that the number of business that terminate within four years is just 24%. And for only 17% of those, “termination” meant failure or bankruptcy — the majority were businesses that were sold or the owner retired.

Sure starting a business is riskier than a job, but these proclamations imply that only an ignorant, greedy, egomaniac would be crazy enough to run into the arms of almost certain failure.

If you’re thinking about starting a new venture right now, you need to understand the risks, but you need the real risks. The truth (as always) lies between these baseless off-hand remarks and those startup blogs that show only the rosy side of things.

First — and bare with me on the pedantry — you have to define “business.” The 2006 US Census [1] shows that half of all “businesses” are a secondary income source, not the primary. More than two-thirds of businesses are started at home; only 21% of all businesses employ someone other than the owner. In other words, most “businesses” are side-projects that the owners might or might not hope will grow into something more.

Not that there’s anything wrong with a side-project! But data about “side projects” isn’t relevant if you’re talking about taking the Big Leap (quitting your job). After all, aren’t side-projects more likely to fail than projects you put all your energy and time and heart and soul into?

Yes, depending on how you define “fail.” An Australian study [2] found that 64% of business fail within ten years if you define “business failure” as “discontinuance of ownership.” But that can mean anything — even if the founder just loses interest which, if you have a home-based business that isn’t your primary income source, could very well be the case.

In the same study, if you define “business failure” as “bankruptcy,” the 10-year failure rate drops to a mere 5.3%! In other words, even when it’s clear that the business isn’t working, bankruptcy is rarely necessary.

What about those long hours you hear about?

Well, that one is true. Every self-employed person I know (myself included) works more than employees (except in those brutal professional sectors like medical services, legal services, and accounting).

Hard numbers: The Canadian government reports that self-employed people work 5 hours more per week than employees. But the real story is this: 33% of self-employed people work over 50 hours, compared to only 5% of employees.

What about making money? NFIB studies routinely report that one-third of all businesses are profitable, one-third are break-even, and one-third lose money.

So here we find some sobering facts. “Losing money” is pretty bad — even being jobless is better than bleeding cash — and “breaking even” isn’t much better. This is real risk, and on top of this I’ll add that you won’t be making money for the first 6-24 months. You need enough money to starve for a while, you have to set financial boundaries for yourself, and you have to walk away if you hit your limits.

However, remember that half of those business are being run part-time. “Hobby” businesses are popular; the fact that someone’s back-room bead-stringing “business” loses money isn’t relevant if you’re thinking about becoming a consultant.

Anyway the real question isn’t “How much money do I expect to gain or lose from running a business?” Rather, it’s “How much money do I expect to gain or lose from running a business compared to my next-best alternative?”

For most people, “next-best” means a job. In a 2006 Gallup survey [3] when small businesses were getting slammed with high gas prices, business owners reported four to one that they make more money per hour than working for another company in the same field. That’s profits, y’all, not revenue. And that’s even with the extra hours small businesses demand.

Furthermore, half of those owners reported that they were earning more through the business than they would have in a regular job, and 76% said they’re better off financially in general:

The US census backs up the “feelings” of these entrepreneurs [4]: In every year between 1990 and 2004, the biggest salaries came from companies with 0-4 employees and companies with more than 500 employees. So if you’re happy slogging it out at a big company, wondering when you might get laid off or have your job shipped overseas, then that’s your best bet at a monthly paycheck. If that doesn’t sound good, tiny companies are the way to go.

But then there’s the economy. Why does everyone think starting a business in a down economy is bad?

Is it because you think no one’s spending money? It doesn’t matter: In your first 6-12 months you won’t have many customers anyway, and those you do get are the most desperate for your product or service. If they’re desperate, it doesn’t matter what the economy is doing.

In fact a bad economy is perfect. Every vendor is hurting: get cheap furniture, cheap rent, cheap advertising, cheap services like art and web design. Good people are out of work; all the better to get help at half-price or a co-founder who just got laid off.

At Smart Bear we just hired a design consultant for 1/3rd of his usual rate. Advertising vendors are dropping their prices without me even asking. Subleases are everywhere as companies try to recoup the cost of their seven-year lease now that they’ve laid off half their staff. It’s prime time to get stuff at low cost.

Here are six reasons to start up in a bad economy. Here’s six more.

But in the end, the real question is one of fulfillment and happiness, not merely of financial success. With a regular job, “happiness” and “money” tend to be inversely related — it’s hard to have both. This is summarized neatly by Juhan Sonin‘s evaluation of his own life:

Running your own business may be the way to break the pattern — both making money and doing what you love — but small business is stressful and difficult and scary. Is it worth it?

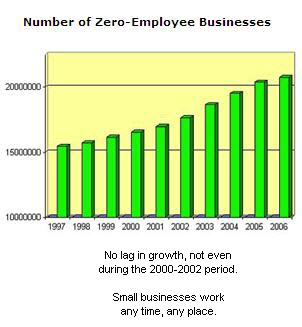

To answer, I’ll leave you with this chart from the Gallup [3] poll:

Hey small business readers! How about sharing your own words of encouragement with other readers of this blog! Inspiring words are great when you’re overwhelmed. Leave a comment!

References:

[1] US Census, 2006 survey of business owners. Data here.

[2] John Watson and Jim E. Everett in Journal of Small Business Management, October 1996

[3] Gallup News Service, 2006 Smart Business Index poll. Came to my attention via the the Corporateprenuer blog

[4] US Census Statistical Abstract 2008 Table 0737. Data via infochimps.org.